From questions to claims, a dedicated C&S account manager is ready to handle all of your car, truck, and motorcycle insurance needs. Let’s get started today.

From questions to claims, a dedicated C&S account manager is ready to handle all of your car, truck, and motorcycle insurance needs. Let’s get started today.

Car Insurance for First-Time Buyers

Buying your first car is exciting—but getting the right insurance is essential to protect yourself and your vehicle. Understanding the types of coverage, state requirements, and your personal needs can help first-time buyers make informed choices while keeping premiums affordable.

Types of Car Insurance

- Liability Coverage: This is the most basic form of car insurance and is usually required by law. It covers the cost of damages and injuries you cause to others in an accident.

- Collision Coverage: This type of insurance pays for repairs to your vehicle in the event of a collision with another vehicle or object, regardless of fault.

- Comprehensive Coverage: Comprehensive insurance protects your vehicle from non-collision-related damage, such as theft, vandalism, or natural disasters.

Other Types of Coverage

The State of Massachusetts also requires you to purchase two additional coverages – personal injury protection (PIP) and uninsured motorist (UM) coverage.

- Personal Injury Protection (PIP): PIP covers medical expenses and lost wages for you and your passengers, regardless of fault.

- Uninsured/Underinsured Motorist Coverage: This coverage protects you if you’re involved in an accident with a driver who either doesn’t have insurance or doesn’t have enough coverage to pay for your damages.

Review Coverage Requirements and Needs

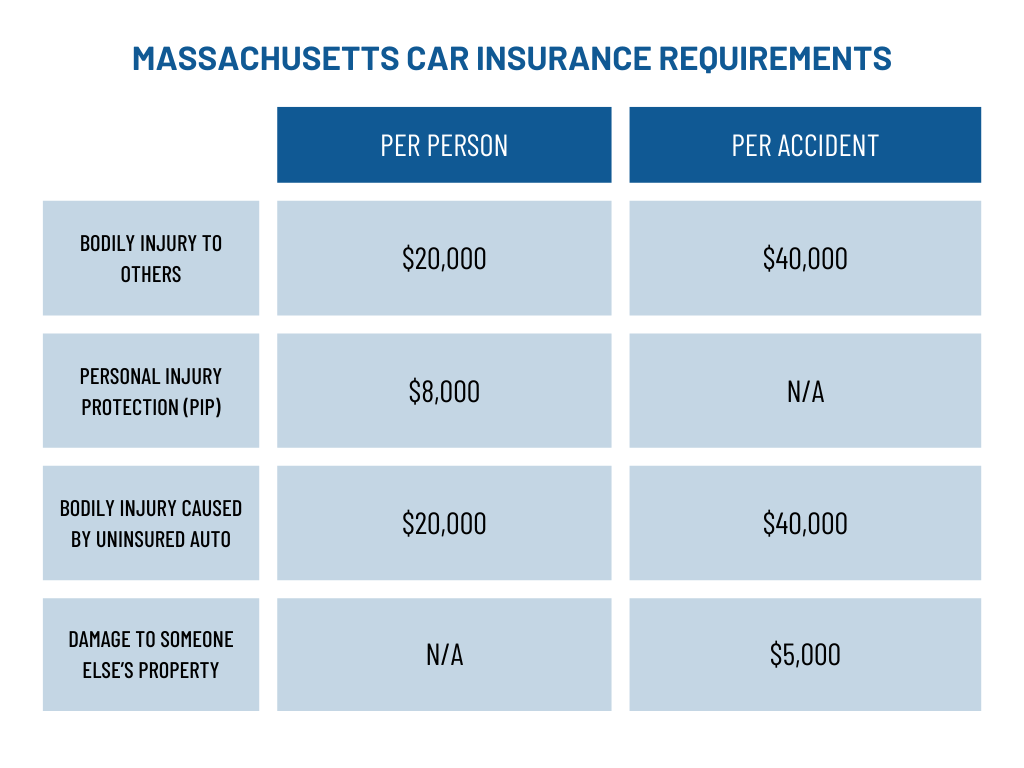

Now that you’re well-versed in the basic types of coverage, you’re ready to dive into your specific car insurance needs. Bay State drivers are required to have four types of car insurance in, at least, the minimum amounts required by law, and in higher amounts if you choose to do so – this is a great starting point when deciding on coverage.

Check out the chart below to see how these compulsory coverages break down:

Keep in mind that if you’re buying your first car insurance policy, you can expect to pay more than a driver who has had insurance for several years. And while driver experience may be an important pricing factor when purchasing car insurance, remember that it’s not the only factor.

Several factors influence the cost of car insurance premiums, including:

- Make/model of car

- Age

- Gender

- Zip code

- Credit history

- Marital status

How to Save Money When Buying Car Insurance

There’s no denying that inflation is having a significant impact on the insurance industry, and owning a car is getting more expensive for drivers nationwide as car insurance premiums surge.

As these insurance costs continue to rise, you may be wondering how you can lower your premium. The good news is that you have options – here are some efficient ways to lower your rate:

- Assess Your Needs: Determine the level of coverage you require based on factors such as your driving habits, vehicle value, and budget.

- Compare Quotes: Shop around and obtain quotes from multiple insurance companies to ensure you’re getting the best possible rate.

- Review Deductibles: Consider how much you’re willing to pay out of pocket in the event of a claim and adjust your deductible accordingly.

- Understand Exclusions: Familiarize yourself with any exclusions or limitations within your policy to avoid surprises down the road.

- Bundle Policies: Many insurance companies offer discounts for bundling multiple policies, such as car and homeowners insurance.

Car insurance is a vital aspect of responsible vehicle ownership, providing financial protection and peace of mind in the event of accidents or unforeseen circumstances. By understanding the different types of coverage, factors affecting premiums, and tips for selecting the right policy, drivers can navigate the road of car insurance with confidence. Remember, the best policy is one that strikes a balance between comprehensive coverage and affordability, ensuring you’re adequately protected no matter where the open road takes you.